January 11, 2024

5 min read

We were unable to process your request. Please try again later. If you continue to have this issue please contact customerservice@slackinc.com.

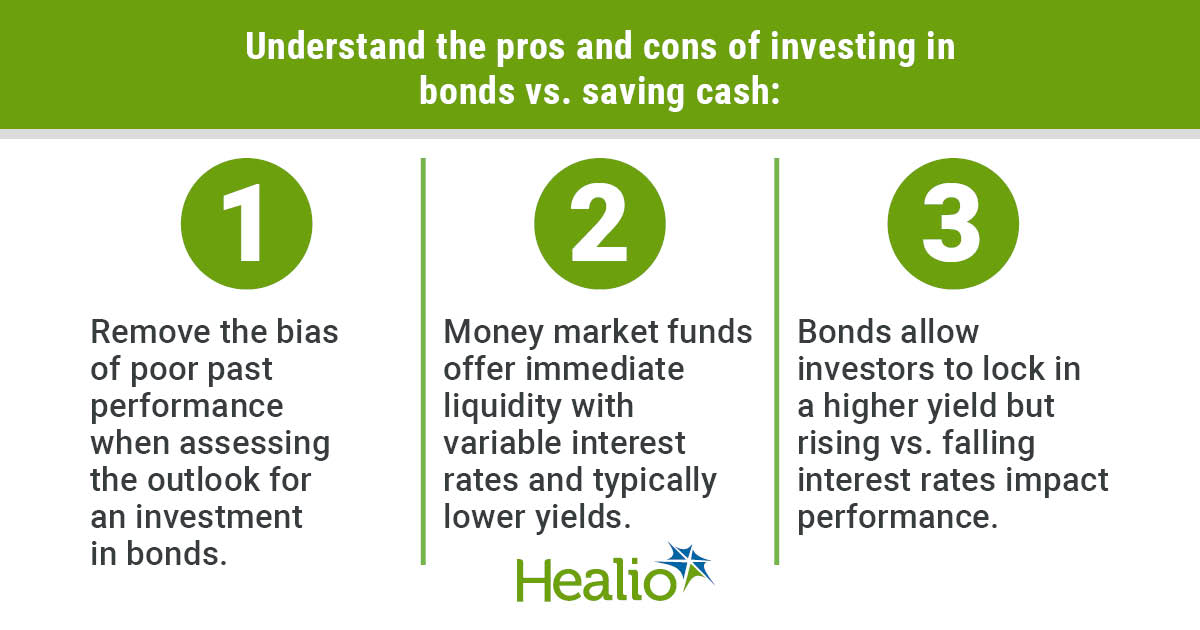

“Why should I be investing in bonds when I can earn more than 5% on my cash?” Many investors, including physicians, are asking this question after being discouraged by losses they have experienced with bonds in recent years.

The question is reasonable, particularly since bonds are intended to limit the downside when stocks sell off. Unfortunately, bonds have recently failed to provide that protection, as these facts confirm:

- From the start of 2022 through the third quarter of 2023, the Bloomberg U.S. Aggregate Bond Index lost more than 14%.

- Longer-term bonds have fared significantly worse. The iShares 20-Year Treasury ETF (TLT) lost nearly 30% during that same period.

- In late October 2023, the TLT had dropped 44% from its high roughly three years prior.

An ETF investing in Treasury bonds (none of which defaulted) lost more than 40% of its value! If we knew for certain the next 3 years were going to look like the last 3, investors would not want to double down on bonds. However, a repeat of the prior 3 years is highly unlikely.

Before providing an outlook on the bond market or comparing the potential benefits of investing in bonds, it may be helpful to understand the factors influencing bond pricing and why bonds experienced losses in 2022 and 2023.

What factors influence bond prices?

While the complete academic answer is a bit complicated, for practical purposes an investor needs to understand the two key factors: credit quality and duration.

David B. Mandell

Andrew Taylor

Credit quality reflects the likelihood that a bond will default. The recent decline in bond prices had little to do with credit quality. Consequently, we will not spend time on this topic, other than to say there is an implied belief that U.S. Treasury Bonds will not default.

Duration is a term used to reference a bond’s sensitivity to the movements of interest rates. A simple way to think about this term is that it reflects how long it takes for your initial investment to be returned.

If you purchase a 5-year bond, your principal will be returned in 5 years. The average maturity of a bond fund is often confused with duration. You are likely to receive interest payments every 3 to 6 months, therefore a portion of your money is returned to you before the end of the 5-year period. The higher the interest rate, the sooner your principal is returned to you. A 5% bond will return your money faster than a 2% bond. Consequently, the 5% bond has a lower duration and is less sensitive to interest rate movements in comparison to the 2% bond.

What happened to bond prices?

Consider an investor purchasing Bond A, a 5-year Treasury Bond for a 2% yield in January 2022 when cash was essentially yielding 0%. One year later, after interest rates skyrocketed, an investor can purchase Bond B, a 4-year Treasury yielding 5%. Yields have been rounded up for simplicity and do not reflect actual yields.

We now have two bonds maturing in 48 months. Let’s assume a $100,000 investment.

- Bond A will pay $2,000 per year and $8,000 over 4 years.

- Bond B will pay $5,000 per year and $20,000 over 4 years.

Bond B is now worth $12,000 more than Bond A; therefore, Bond A will need to be repriced accordingly in the public markets. Investors in Bond A will have a significant paper loss in the calendar year; however, owners of both Bond A and Bond B will receive their initial $100,000 investment in 48 months.

The following year each bond has 3 years of interest payments remaining and Bond B will pay $9,000 more in interest than Bond A over the remaining life of the bond. Naturally, the difference in value between the two bonds has changed. Bond A will increase in value to reflect the difference in…

Read More: Understand the pros and cons