In the past year, South Korea’s market has shown a modest uptick, increasing by 6.0%, with a stable performance over the last week and earnings expected to grow by 30% annually. In such an environment, growth companies with high insider ownership can be particularly compelling, as this often signals confidence from those who know the company best.

Top 10 Growth Companies With High Insider Ownership In South Korea

|

Name |

Insider Ownership |

Earnings Growth |

|

ALTEOGEN (KOSDAQ:A196170) |

26.6% |

73.1% |

|

Global Tax Free (KOSDAQ:A204620) |

18.1% |

72.4% |

|

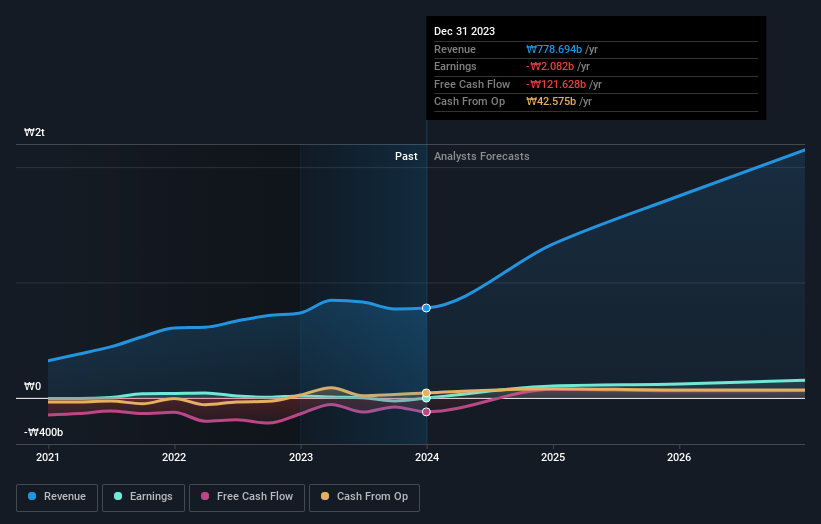

Seojin SystemLtd (KOSDAQ:A178320) |

26.2% |

48.1% |

|

Fine M-TecLTD (KOSDAQ:A441270) |

17.3% |

36.4% |

|

Park Systems (KOSDAQ:A140860) |

33.1% |

34.3% |

|

UTI (KOSDAQ:A179900) |

34.1% |

122.7% |

|

Vuno (KOSDAQ:A338220) |

19.5% |

105% |

|

HANA Micron (KOSDAQ:A067310) |

20% |

96.3% |

|

INTEKPLUS (KOSDAQ:A064290) |

16.3% |

77.4% |

|

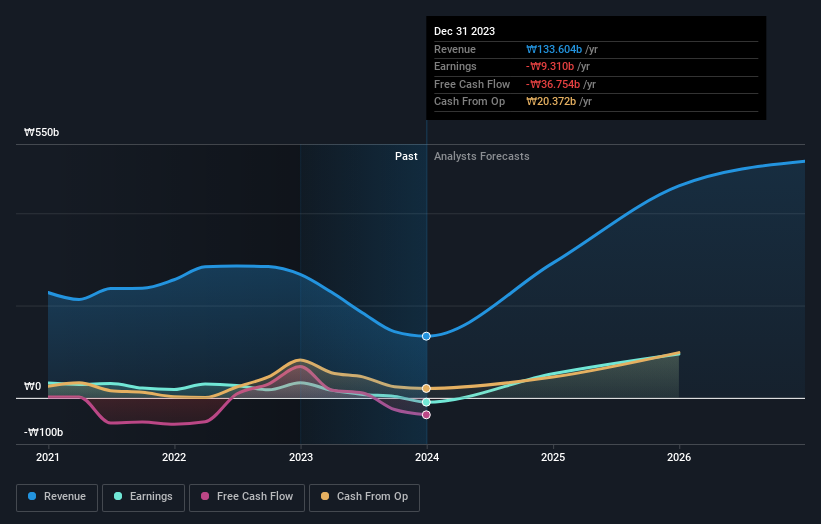

Techwing (KOSDAQ:A089030) |

18.7% |

77.8% |

Let’s take a closer look at a couple of our picks from the screened companies.

Simply Wall St Growth Rating: ★★★★★★

Overview: Techwing, Inc. operates globally, focusing on the development, manufacturing, sale, and servicing of semiconductor inspection equipment, with a market capitalization of approximately ₩2.41 trillion.

Operations: The company’s primary revenue is generated from the development, manufacturing, sale, and servicing of semiconductor inspection equipment.

Insider Ownership: 18.7%

Earnings Growth Forecast: 77.8% p.a.

Techwing, a South Korean company, is poised for significant growth with an expected revenue increase of 41.3% annually, outpacing the domestic market’s 10.7%. Despite challenges in covering interest payments with earnings and a highly volatile share price recently, its forecast to turn profitable within three years is promising. Additionally, insider ownership remains robust though specific recent trading data is unavailable. Notably, its projected Return on Equity of 33.1% underscores potential financial efficiency improvements ahead.

Simply Wall St Growth Rating: ★★★★★★

Overview: Seojin System Co., Ltd specializes in manufacturing telecom equipment, repeaters, mechanical products, and LED equipment, with a market capitalization of approximately ₩1.88 billion.

Operations: The company generates revenue primarily through its EMS segment, which brought in ₩1.22 billion, and its semiconductor operations, contributing ₩0.16 billion.

Insider Ownership: 26.2%

Earnings Growth Forecast: 48.1% p.a.

Seojin System Ltd, despite its challenges with earnings coverage for interest payments and a recent dilution of shareholders, shows promising growth potential in South Korea. The company’s earnings are expected to grow by 48.06% annually, significantly outpacing the KR market average. Additionally, revenue forecasts indicate a 28.5% annual increase, also above market trends. However, investors should note the highly volatile share price and lower profit margins compared to last year. Analysts predict a substantial rise in stock value, trading at US$54.4% below estimated fair value.

Simply Wall St Growth Rating: ★★★★★☆

Overview: Enchem Co., Ltd. is a South Korean company engaged in the production and sale of electrolytes and additives for secondary batteries and electric double-layer capacitors (EDLC), with a market capitalization of approximately ₩4.81 billion.

Operations: The company generates revenue primarily from its electronic components and parts segment, totaling ₩357.37 million.

Insider Ownership: 19.8%

Earnings Growth Forecast: 144.8% p.a.

Enchem, despite recent shareholder dilution and a highly volatile share price, is poised for significant growth in South Korea. The company’s revenue is expected to increase by 56.5% annually, surpassing the market average significantly. Additionally, Enchem is forecasted to turn profitable within the next three years, an outlook that outpaces general market expectations. However, there’s a lack of recent insider trading data to confirm ongoing confidence from insiders directly.

Taking Advantage

Want To Explore Some Alternatives?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company…

Read More: KRX Growth Companies With High Insider Ownership And 144% Earnings Growth