Mihaela Rosu/iStock via Getty Images

While the stock market is making new highs and those of us who are recently retired or are soon to retire are enjoying a healthy income stream from high yield investments such as those described in my recent Income Compounder portfolio update, it may be prudent to consider risk management. If the market sentiment shifts this summer as some are predicting and we experience a correction of 5% or more, it may be wise to raise some cash or at least hold a portion of your investment portfolio in relatively “safe” lower yielding securities.

I realize that this topic may not garner as much attention as some of my recent posts which tend to highlight opportunities to generate massive amounts of cash flow from high yielding funds such as Oxford Lane Capital (OXLC), a CEF that I recently reviewed that now yields about 20% after raising their dividend in May. The tendency to “chase yield” as some like to say, may be exciting and opportunistic but can also lead to capital losses when the market turns. On the other hand, buying those high yield funds during a market correction can lead to even stronger returns over time. In that case, it may make sense to hold some “dry powder” in the form of cash or liquid funds that can be easily and quickly converted to cash to take advantage of those buying opportunities.

In this article, I would like to suggest another fund that invests in CLOs but carries less risk of substantial capital depreciation in the event of a market downturn. Of course, lower risk also comes with lower returns and unlike OXLC the yield from Janus Henderson B-BBB CLO ETF (BATS:JBBB) currently amounts to about 7.8%. I consider JBBB one example of a cash-like fund that offers a higher yield than most money market funds and carries relatively low risk of capital losses.

In my own IC portfolio, I currently hold about 10% of my total portfolio value in several funds that carry less risk than the high yielders that I typically cover but still offer higher yields than the typical money market funds that yield about 5%. As the market continues to make new all-time highs, I am starting to take profits from some of my investments that have large unrealized gains and putting those profits into cash (including Fidelity’s money market sweep account, SPAXX, 4.95% yield) and lower risk holdings including SGOV (5.2%), IBHF (7.4%), and JBBB. My intent is to increase my cash and lower risk holdings to closer to 20% of my total in anticipation of a market correction.

Why JBBB and Why Now?

From the website, this is the About JBBB description of the fund:

An ETF with floating rate exposure to CLOs rated from B to BBB and seeking to deliver investors access to securities with low default risk, low correlations to traditional fixed income asset classes and yield potential.

The inception date for JBBB was January 2022 and it has about $920M in total net assets.

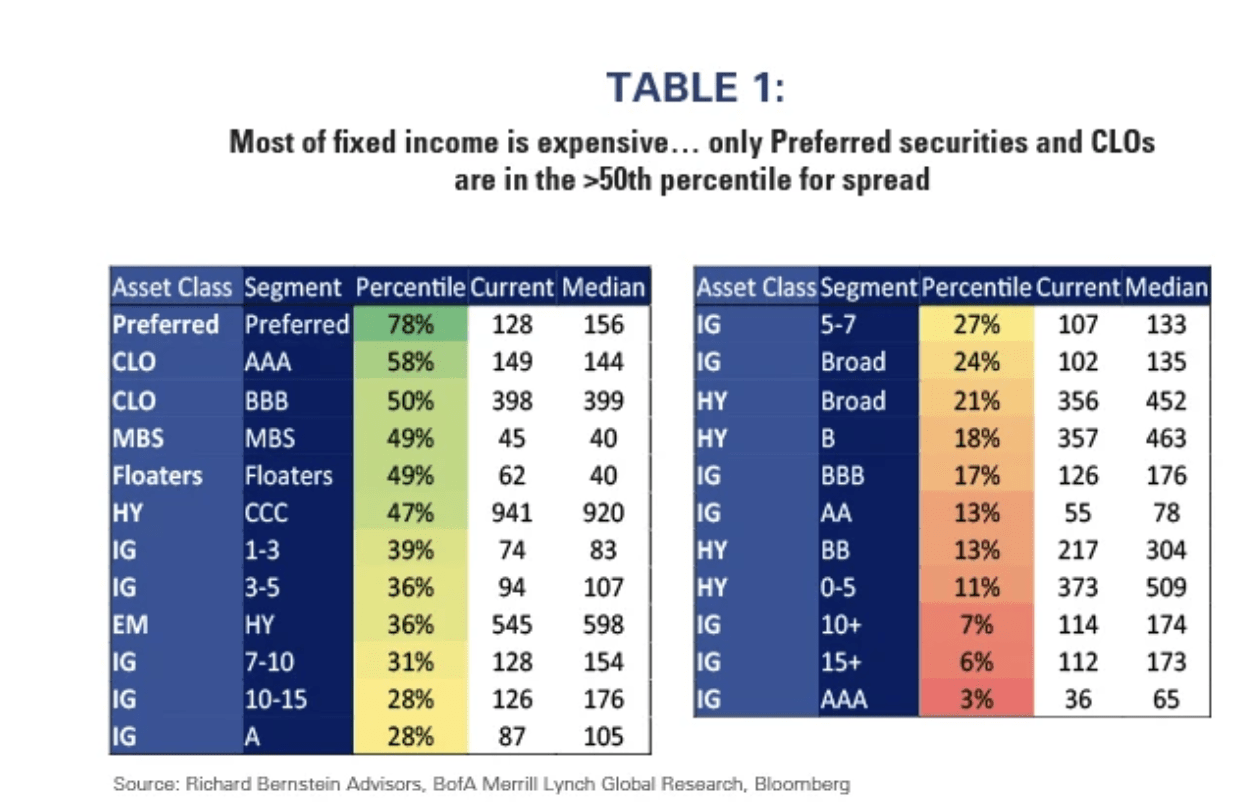

As explained in this recent insight from RBA the best risk-reward in fixed income investments is in Preferred Securities and CLOs.

At the top of the list are those sectors that currently trade with a reasonable yield spread from a historic percentile basis, suggesting reasonable risk-reward. Preferred Securities, AAA and BBB CLOs, and agency mortgage-backed securities lead the pack in terms of their attractiveness. On the bottom resides longer duration and high-quality investment grade corporates and short duration high yield corporates.

RBA

In general, CLOs offer an attractive risk-reward with higher yields at lower relative risk than other fixed income investments such as senior loans or corporate bonds. This discussion by Van Eck titled, CLOs: Too Good to be True? explains some of the advantages of CLOs in terms of high yield and some of the structural protections that make them low risk.

High yielding collateral: CLOs are backed by a pool of leveraged loans, which are non-investment grade and produce high levels of income that gets distributed to CLO tranche investors. As of February 29, 2024, leveraged loans yielded 9.2% versus 5.5% on investment grade corporate bonds.

Structural protections: Each tranche of a CLO has varying degrees of subordination, which insulates investors from default losses. Active management, collateral requirements, and overcollateralization provide additional protection. Combined with the lower loss rates on senior secured loans relative to high yield bonds, the risk of default in investment grade CLO tranches is negligible. The average CLO portfolio would need to experience default rates several multiples of the historical average, for 5 or more consecutive years, for the first dollar of loss even in BBB and BB rated tranches. There has never been a default in AAA rated CLOs.

What…

Read More: JBBB ETF: Balancing Risk Versus Reward (BATS:JBBB)