MicroStockHub/iStock via Getty Images

This is a short article which takes a careful look at the mainstream narrative that Bitcoin ETFs signal institutional adoption, and that Wall Street is increasingly bullish on Bitcoin (BTC-USD). It’s been three months since the spot ETFs were approved, and we’ve seen a good amount of activity from these funds. BlackRock’s iShares Bitcoin Trust ETF (IBIT) has been called the most successful ETF launch in history by Larry Fink. There were prominent headlines when IBIT surpassed MicroStrategy (MSTR) in the amount of BTC held.

The sentiment within crypto circles seems to be that Wall Street is entering the game and that things are only going up from here. I just want to do a quick reality check on whether Wall Street is actually as bullish on BTC as people are saying. Based on what I have seen, I don’t think the ETF net inflows indicate Wall Street is bullish at all. We need to consider the net inflows because Grayscale Bitcoin Trust ETF (GBTC) has seen a huge amount of outflows.

Here Are The Numbers

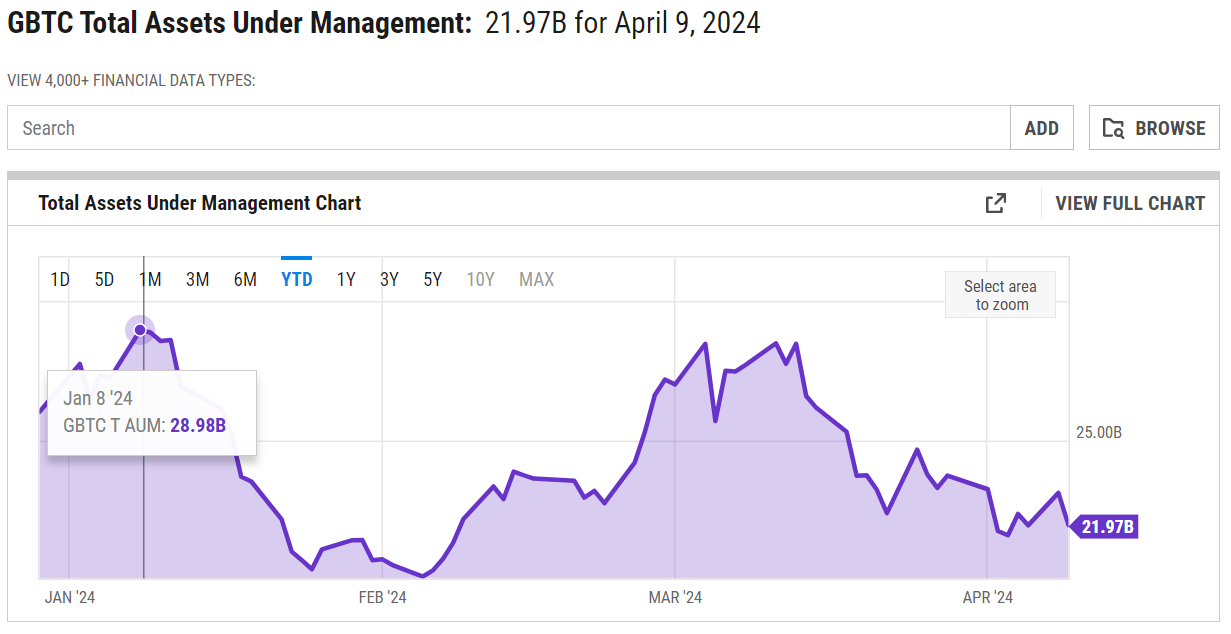

Right before the approval of the spot ETFs, GBTC had about $29 billion in AUM. The BTC price on January 8 2024 was about $47,000. This means GBTC held about 617,000 BTC.

GBTC AUM (YCharts)

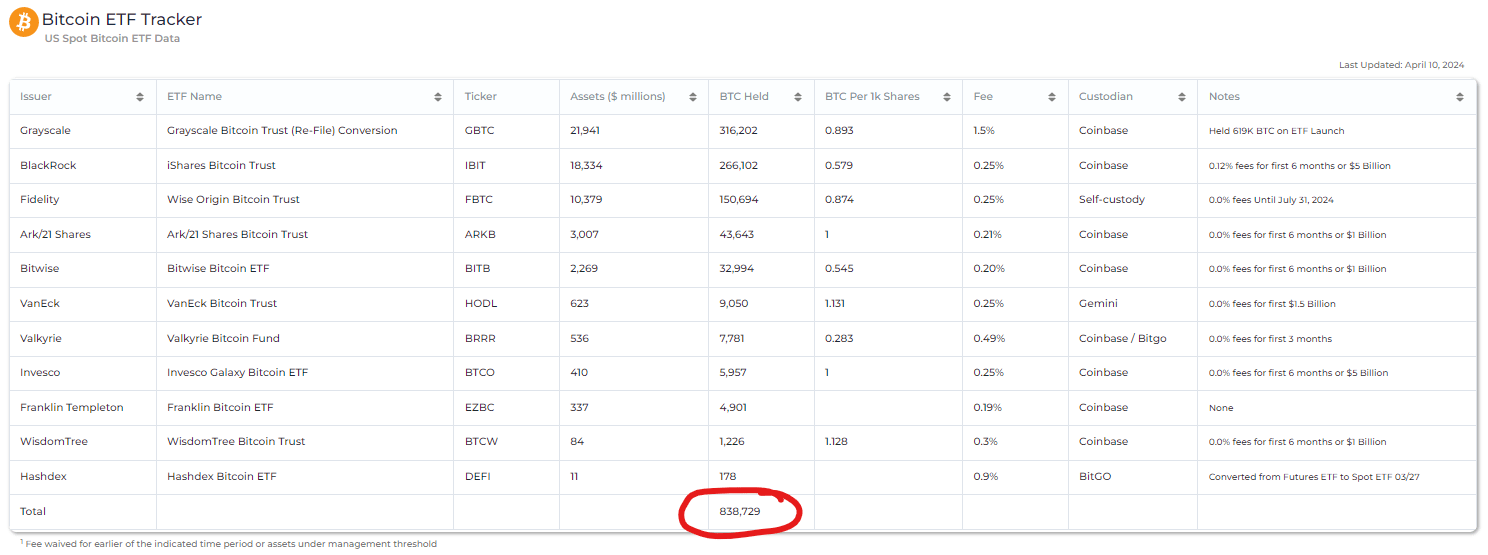

As of April 10 2024, the combined Bitcoin ETFs hold 838,729 BTC. Let’s round this number to 839,000 BTC.

Bitcoin ETFs (heyapollo.com)

So we started with only GBTC’s 617,000 BTC and now there are 839,000 BTC in all the funds, so it looks like Wall Street is super bullish right? Investors clearly bought up a net 222,000 BTC during this time – more than 1% of the entire maximum supply of 21 million BTC, and just slightly higher than MicroStrategy’s total BTC holdings. This is used by those in crypto to show that there is “insatiable demand” for BTC from Wall Street, and that ETFs are literally “eating multiples of the daily issuance of BTC.”

Not so fast.

Kerrisdale recently published a “short report” on MicroStrategy. Even though it was called a short report by the media, it was actually outlining a simple pairs trade between MSTR and BTC. Their thesis is that MSTR has become overvalued compared to the BTC it holds, trading at an unsustainably high premium, so it is time for a long BTC, short MSTR pairs trade.

Now I think it should be quite obvious that Kerrisdale, or any other hedge fund making this bet, will use a Bitcoin Spot ETF as the “long BTC” leg of this pairs trade. ETFs are marginable securities, whereas real BTC cannot be margined in a brokerage account. It is much more capital efficient for a trader to use the ETFs and manage the risk within a single account. Even today when brokers offer crypto, they are actually enlisting the help of other firms which specialize in custodying and transacting crypto. The spot ETFs are the best option, and I believe many hedge funds may be betting on this trade, so they are inherently long BTC via the ETFs.

Importantly, these longs are not long because they are bullish on BTC. They are long only to capture a spread between MSTR and BTC. Such traders do not have any interest in BTC, yet they will nevertheless show up as ETF inflows.

In other words, at least some of the 222,000 BTC inflow is due to traders needing a marginable long BTC position while shorting MSTR.

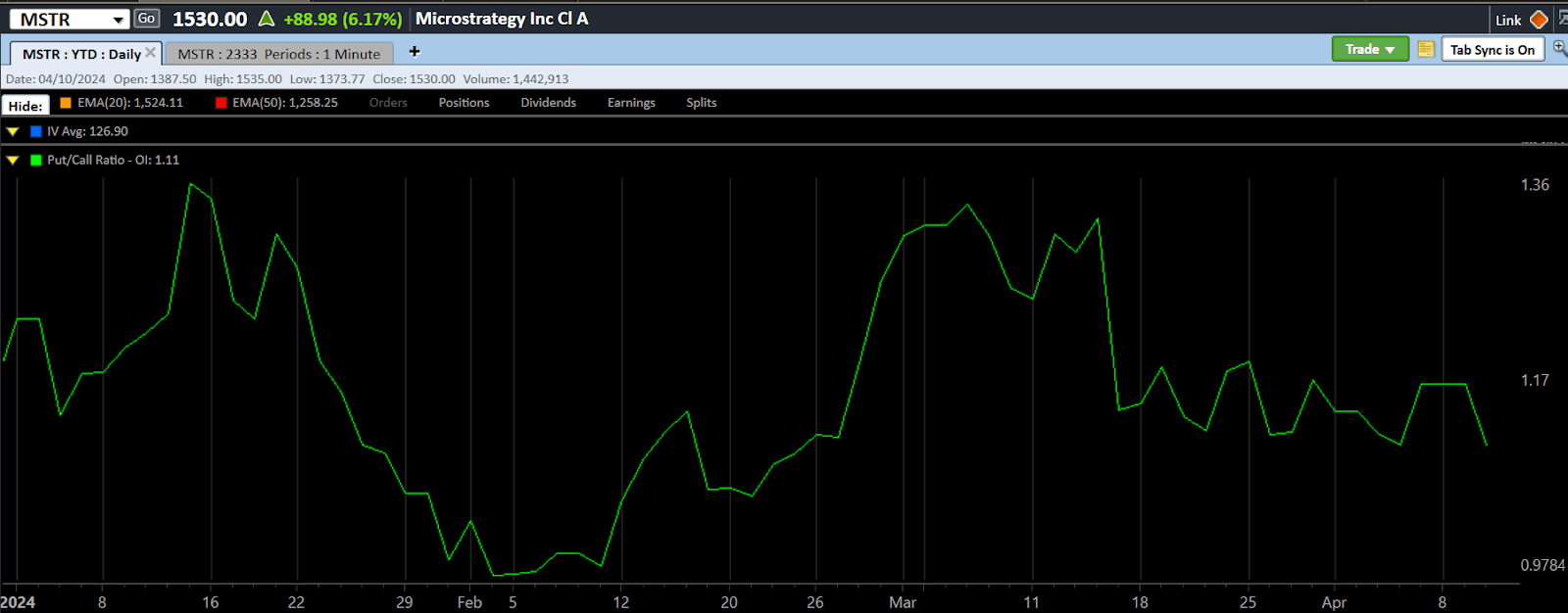

How much dollars might be betting on this? Well, the short interest on MSTR is about 19% of outstanding shares. Let’s assume some of these are unhedged shorts and others have to do with the convertible debt issuance. I also think that some hedge funds will do this long/short but use MSTR options for the short position. This is effectively a “synthetic short” position which won’t show up on the short interest. They could sell a call and buy a put. Indeed, the puts to call ratio for open interest has been approaching 1, indicating that roughly the same amount of contracts exist for both puts and calls.

MSTR Puts/Calls OI (Schwab)

Assuming much of the short interest is betting on this pairs trade, and assuming that derivatives are used for some of the MSTR shorts (thus obfuscating and understating the true amount of short positions), I’m guessing maybe 20% of the shares outstanding in notional short value in this pairs trade exists – as a combination of options and shares sold short. Personally I think 20% is a conservative figure.

There’s more. The market cap of MSTR is $26.3 billion and they hold 214,246 BTC, worth about $14.8 billion. So the premium over owned BTC is about 78%. So to get a dollar-equivalent MSTR/BTC pairs trade, you’d need to be long about 1.78x as much BTC as what the MSTR shares you are shorting is supposed to represent. For example, 100 MSTR shares represent 1.26 BTC held by MicroStrategy. But 100 MSTR shares is worth about 2.24 BTC,…

Read More: Bitcoin Reality Check: Wall Street Doesn’t Seem Bullish Despite ETFs