hansenn/iStock via Getty Images

By Andrew Prochnow

It’s been nearly 30 years since the Federal Reserve pulled off the last “soft landing” in the U.S. economy.

Back in the mid-1990s, the Federal Reserve raised benchmark interest rates to fight inflation, much as it has done over the last couple of years. And once inflation was tamed, the Fed proceeded to gradually lower rates back to “normal” levels.

That period is often viewed as a “soft landing,” because the Fed successfully raised rates without crashing the economy. The central bank was also largely successful in its goal to rein in inflation.

In 2024, the Fed is attempting to thread the needle on rates and inflation for the second time in 30 years. And this is a critical period for stock market investors, because the stock market has historically responded very differently to soft and hard landings.

As most investors and traders are well aware, the last two hard landings in the economy were the “dot-com bubble” and the “Great Recession,” both of which involved sharp corrections in the stock market.

In contrast, the “soft landing” in the mid-1990s produced far more attractive returns in the stock market, largely because the economy avoided falling into recession. That will undoubtedly be a key to success this time around, as well, with the Federal Reserve hoping it can maintain positive growth in the economy during the next 6-12 months.

As it did back in the mid-1990s, the Fed is expected to gradually lower benchmark interest rates in 2024 to help foster a gradual rebound in the economy. During the Fed’s December policy meeting, central bankers intimated they will cut rates as many as three times this year.

Today, the current target range for the country’s primary interest rates benchmark—the federal funds rate—is 5.25-5.50%. Three rate cuts of a quarter percentage point each would consequently drop that range to 4.50-4.75%.

The net amount of expected cuts—approximately 0.75%—is almost identical to the degree to which the Fed cut rates back in the mid-1990s. From June of 1995 to February of 1996 the effective federal funds rate fell from roughly 6% to about 5.2%.

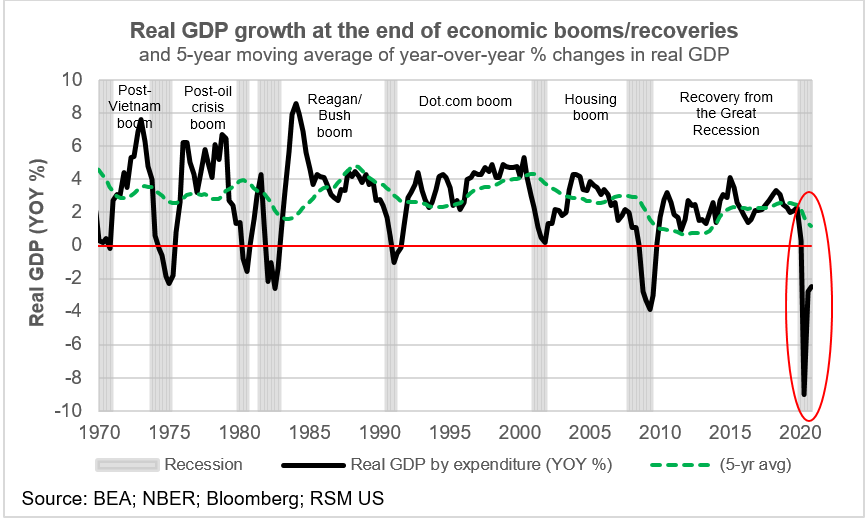

Importantly, the gross domestic product (GDP) of the United States continued to grow during that period. From 1994 to 1997, the lowest quarterly GDP growth rate for the United States was +2%. And when the Fed started cutting rates in the summer of 1995, GDP growth actually surged back toward +4%, as highlighted below.

Road to recovery

Much like in the mid-1990s, the Fed is anticipated to gradually reduce benchmark interest rates in 2024 to facilitate a measured economic recovery. During the December policy meeting, central bankers indicated an intention to implement up to three rate cuts within the year.

Presently, the targeted range for the nation’s primary interest rates benchmark—the federal funds rate—is 5.25-5.50%. If three quarter-point rate cuts are executed, this range would consequently contract to 4.50-4.75%. The cumulative magnitude of anticipated cuts, approximately 0.75%, closely mirrors the extent to which the Fed reduced rates in the mid-1990s. From June 1995 to February 1996, the effective federal funds rate declined from around 6% to approximately 5.2%.

Significantly, the gross domestic product (GDP) of the United States continued to expand during that period. Between 1994 and 1997, the lowest quarterly GDP growth rate for the United States was +2%. Notably, when the Fed initiated rate cuts in the summer of 1995, GDP growth experienced a resurgence, moving back towards +4%, as highlighted below.

{kind=link}

In hindsight, many economists refer to the mid-1990s as the “perfect” soft landing. It’s also arguably the “only” successful soft landing that’s been observed in modern economic history

In 2024, the Fed is poised to try and pull off another soft landing, and if it does, it will probably be regarded as “perfect,” too. Because any rate hike cycle that doesn’t result in a recession/depression is likely to be remembered as an ideal outcome.

One of the big things the U.S. economy has going for it this time around has been its resilience. Even in the face of sharply higher interest rates, the U.S. economy has continued to grow. Back in the mid-1990s, the U.S. economy exhibited similar strength, which is why these two periods have drawn so many comparisons in recent months.

If the U.S. economy does avoid falling into recession during the next 6-12 months, it’s highly likely the stock market will avoid a sharp correction, as well.

How the Stock Market Has Historically Responded to Soft and Hard Landings

At the start of a new trading year, most investors and traders are concerned with the direction of the stock market. And based on historical returns in the stock…

Read More: Why A Soft Landing Is So Bullish For The Stock Market (SP500)