2d illustrations and photos

I last wrote on the Vanguard FTSE Emerging Markets Index Fund ETF (NYSEARCA:VWO) in July last year, where I argued rising bond yields relative to the index’s dividend yield no longer justified a bullish position. Since then, the VWO’s yield has declined while Treasury yields have risen further. Furthermore, the weighting of China has fallen due to falling valuations of Chinese stocks, which has left investors with heavy exposure to the Indian and Taiwanese markets, which are looking increasingly stretched. I continue to rate VWO as a ‘hold’ but would use any strength to shift into Chinese stocks, which are now underrepresented in the ETF.

The VWO tracks the performance of the FTSE Emerging Markets All Cap China A Inclusion Index. The VWO boasts a very low expense ratio of 0.1%, which compares favourably to the 0.7% charge for the iShares MSCI Emerging Markets ETF (EEM). Another key difference between the two ETFs is the absence of Korean stocks in the VWO, which has the effect of increasing concentration in China, India, and Taiwan. This also has the effect of reducing exposure to information technology. The VWO is also slightly more diversified in terms of its single company exposure, with the top 10 stocks making up 17% of the VWO versus 23% for the EEM.

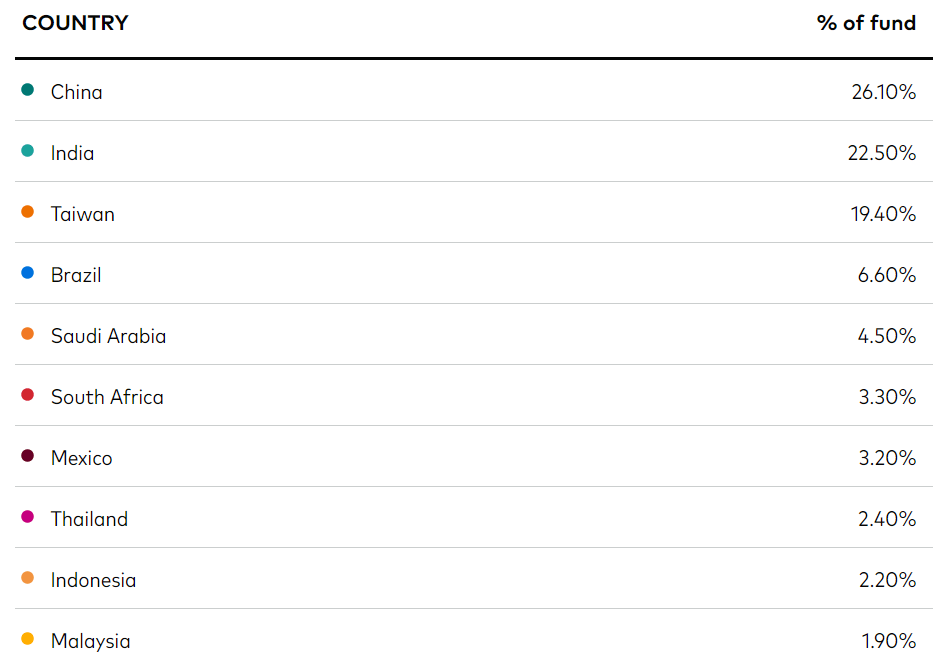

Less than a year ago, China’s weighting was around three times that of India, and double that of Taiwan, but the decline in Chinese stock valuation multiples and the rise in multiples in India and Taiwan have shifted the ETFs weightings considerably. China’s weighting is now just 26%, only just ahead of India at 22.5% and Taiwan at 19.4%. By company, Taiwan Semiconductor (TSM) waiting in the index has risen to 5.8%, making it by far the largest stock in the ETF.

VWO Country Weightings (Vanguard)

{kind=link}

Valuation Multiples Look Stretched Despite China’s Derating

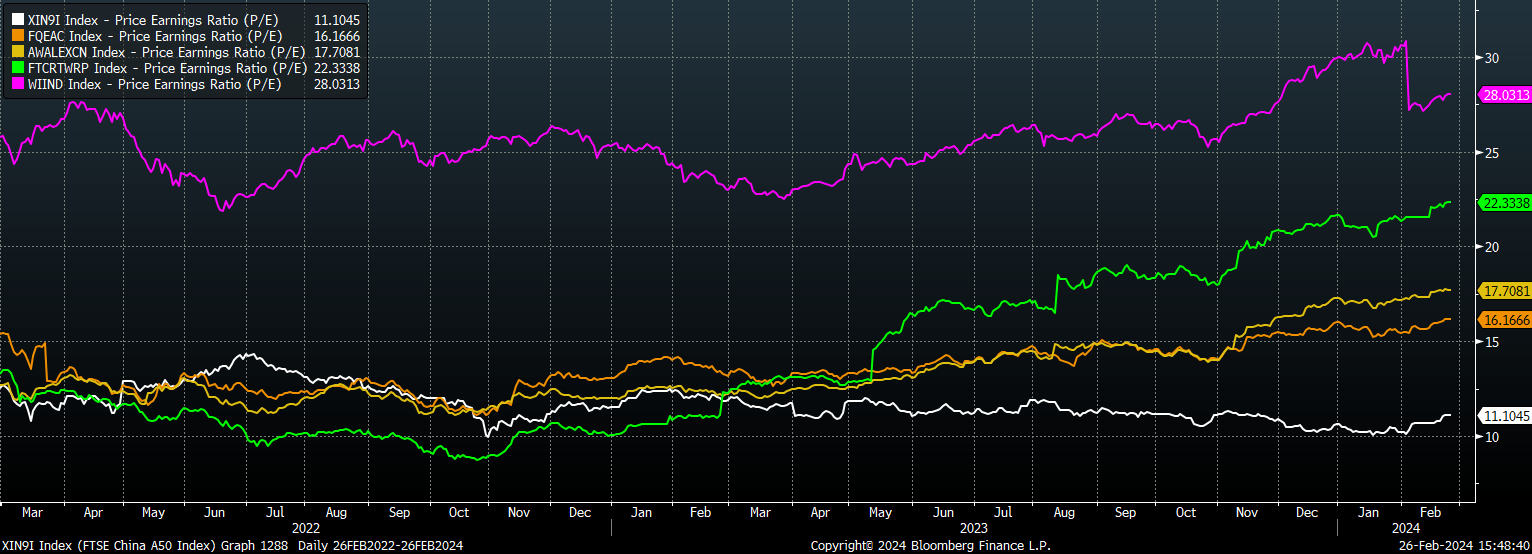

The rise of Indian and Taiwanese stocks has seen the valuation multiples for the FTSE Emerging Markets All Cap China A Inclusion Index rise to multi-year highs even as Chinese stock valuations have continued to decline. The trailing PE ratio for the index is over 16x, while the EV/EBITDA multiple is up at 10x. Both of these figures are back above pre-Covid peak levels.

The following chart shows PE ratios for the FTSE China Index (white line), the FTSE Emerging Markets Index (orange line), the FTSE Emerging Market Ex-China Index (yellow line), the FTSE Taiwan Index (green line), and the FTSE India Index (purple line). India and Taiwan have dragged up the valuation multiples of the VWO even as Chinese stocks have become extremely cheap.

PE Ratios Across EM Indices (Bloomberg)

{kind=link}

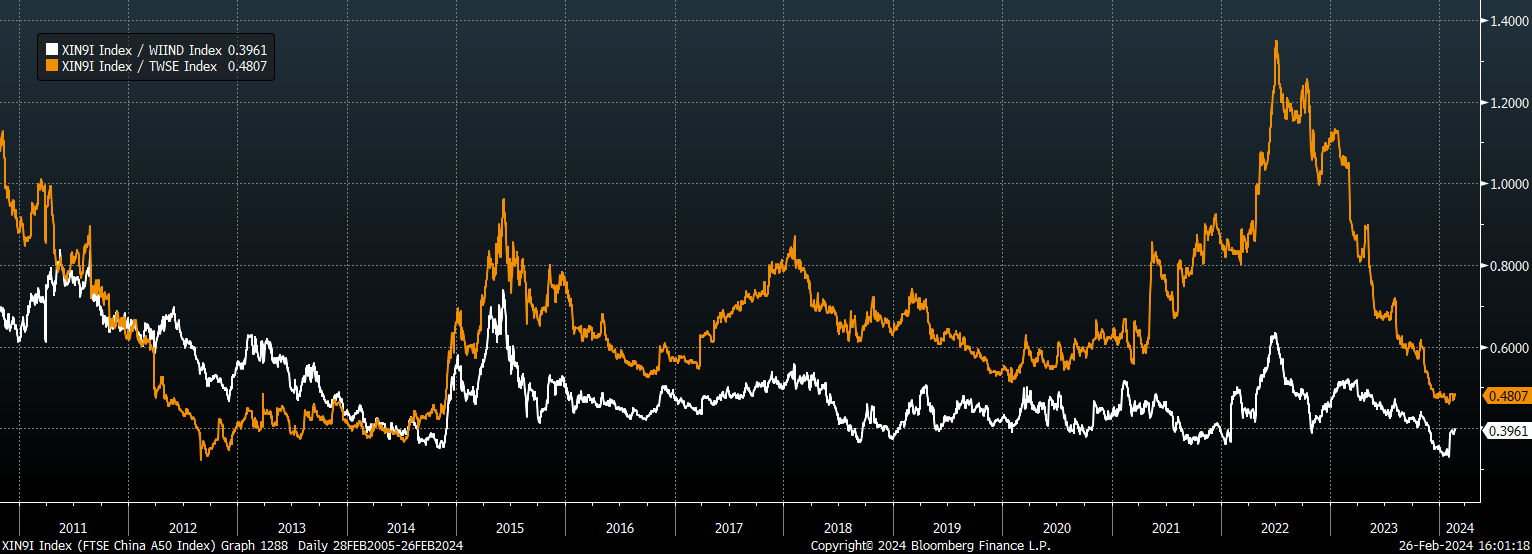

Looking longer term, China has rarely been this undervalued relative to India and Taiwan, currently trading at a 60% discount to India and 52% discount to Taiwan on a trailing PE basis.

Ratio of China PE Ratio Vs Taiwan (Orange line) and India (White line) (Bloomberg)

{kind=link}

As this article explains, there has been a rise in EM focussed ETFs that exclude China over the past year, with investors shunning China exposure amid the market’s decline due to fears of stagnant growth, rising China-US tensions, and the threat of government intervention. In contrast, India has seen a surge in investment interest over the past year. As the chart below of India versus China fund flows over the past year shows, being long China versus India is certainly going against the crowd. In my view, investors should be taking advantage of undervalued and unloved Chinese stocks by raising allocations rather than reducing them, and should be taking profit on Indian and Taiwanese stocks rather than increasing allocations.

Bloomberg

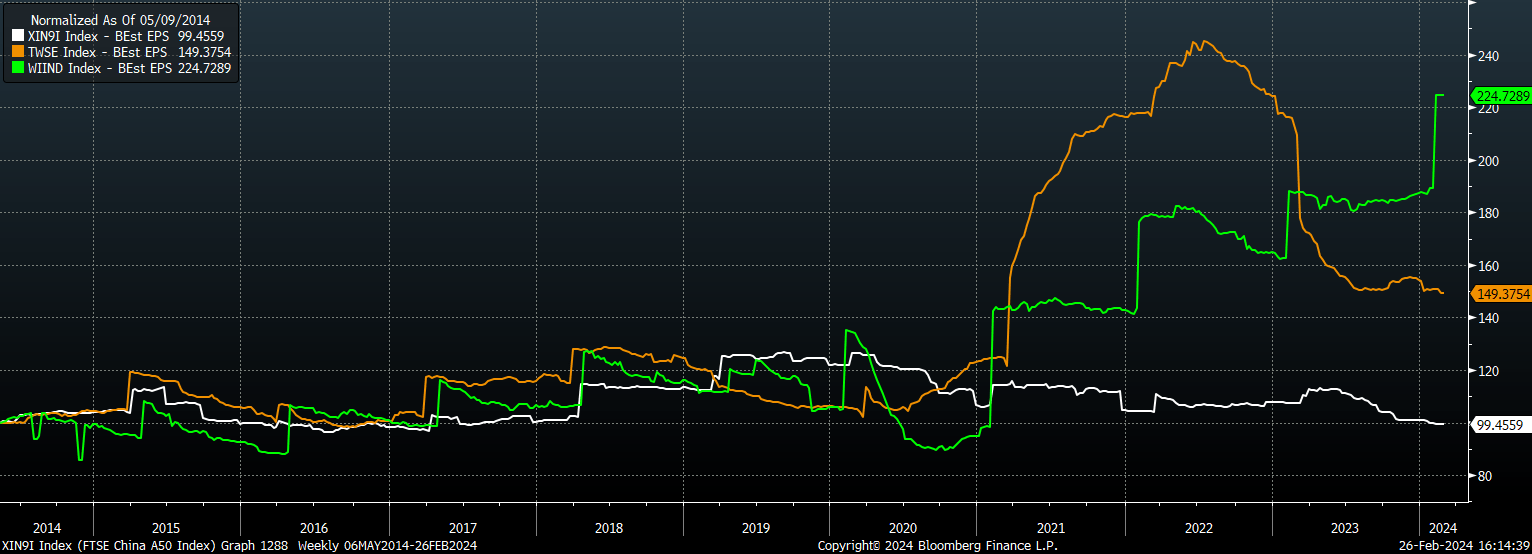

The main risk to this view of VWO underperformance relative to China that Chinese fundamentals continue to underperform in line with recent trends. As shown below, forward earnings expectations for India (green line) and Taiwan (orange line) have significantly outperformed China (white line).

Forward Earnings Expectations (Bloomberg)

{kind=link}

However, even on a forward basis, Chinese stocks trade at around half the earnings multiples of Taiwan and India, which would require Chinese profits and dividends to grow significantly slower indefinitely in order to be justified.

Summary

China’s weighting in the VWO ETF has fallen significantly over the past year, particularly at the expense of India and Taiwan, which has been driven mainly by China’s relative valuation multiple contraction. While Chinese stocks are now undervalued, the VWO does not have enough exposure to them to justify a buy rating, given how high the weighting of expensive Indian and Taiwanese stocks has become in the ETF.

Read More: VWO ETF: Declining China Exposure To Hurt Returns