The Upward Trajectory of Silver Demand

Global silver demand is poised to rise to 1.2 billion ounces in 2024, potentially marking the second highest demand level on record, driven predominantly by industrial applications. The projected 4.0 percent rise in silver industrial fabrication this year will underpin the growth in demand, reaching a peak of 690 million ounces—a testament to the white metal’s enduring industrial importance.

However, forecasts of rising demand are driven mainly by the rapidly expanding electric vehicle (EV) market, and with it, silver’s utilization in electronic components and the burgeoning battery charging infrastructure that will be needed to support the increased use of electric vehicles.

{kind=link}

The integration of AI into consumer electronics holds promise for silver usage, as tech companies prepare to launch new silver-intensive products into the market.

Additionally, a notable revival in the jewelry and silverware sectors is expected to inflate demand by 6.0 percent, with India playing a pivotal role in the market uplift. The jewelry sector, in particular, anticipates a resurgence in demand, based in the view that India’s economy presents a conducive environment for growth.

However, the U.S. and European jewelry markets might continue facing headwinds from cautious consumer spending, partially offset by retailers’ inventory rebuilding efforts.

In 2023, the U.S. silver mining industry thrived with production reaching approximately 1,000 tons. Alaska and Nevada lead the charge in silver output, demonstrating the continued relevance of silver in the national mining landscape.

Silver’s role in the U.S. stretches across many sectors—from investment bars and electrical components to coins and medals, demonstrating its versatility and durability as an industrial and investment asset.

The U.S. continues to engage actively in the international trade of silver, boasting consumption patterns that reflect its robust industrial landscape and investment strategies.

However, silver recycling is expected to drop to by 3.0 percent. This retracement is largely due to diminishing returns from jewelry and silverware scrap, coupled with a sustained decline in photographic scrap supply.

Silver supply may face obstacles, particularly from the by-product production from base metal mines, which is expected to decrease in the wake of mine closures stemming from societal and governmental disputes, particularly in South America.

As 2024 unfolds, financial markets are readjusting their expectations regarding U.S. interest rate cuts, and how this might influence the price of silver. Although an initial rise in U.S. rates seems unlikely, expected adjustments in the latter half of the year suggest potential for silver investment recovery.

Investment dynamics as in relation to silver are intricately linked to global economic policies. With the U.S. Federal Reserve poised to start rate cuts by mid-year, silver could be bolstered as inflation abates, real yields fall, and the dollar faces pressure.

The contrasting economic landscapes of the U.S. and China will play a pivotal role in silver investment trends. A robust U.S economy might suppress investment in silver, while a lagging recovery in China could similarly act as a deterrent.

While initial forecasts for 2024 remain cautious about the outlook for investment in precious metals, particularly silver, a turnaround is anticipated when the Federal Reserve triggers rate cuts. Investment trends in silver for the latter part of the year are expected to pivot, enhancing the metal’s attractiveness as a hedge against volatility, particularly if economic signals point towards monetary easing and inflation targeting.

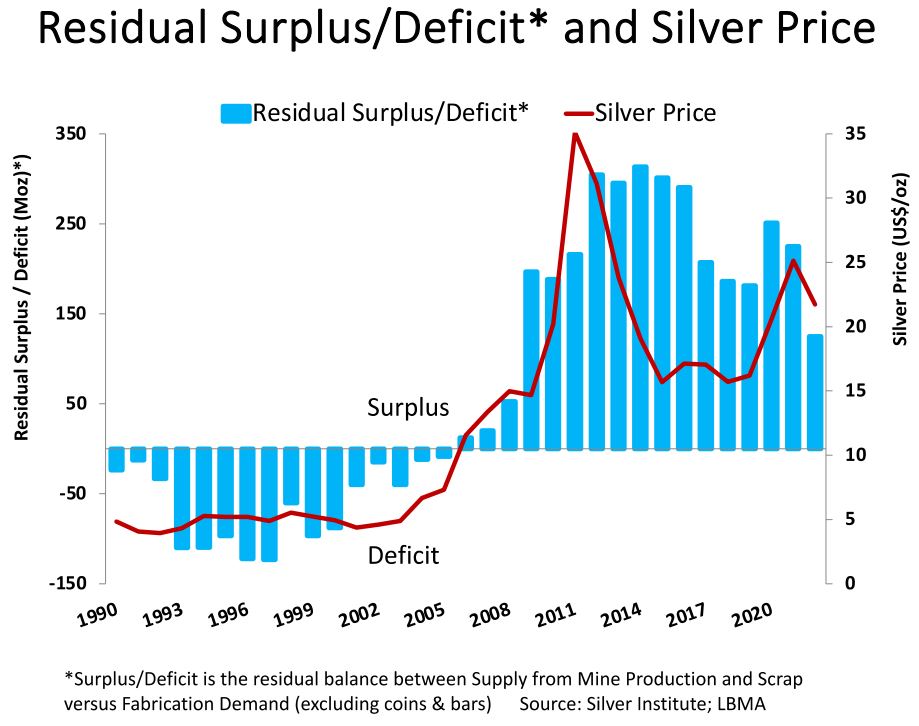

A projected easing of inflation and real yields could stimulate investment in silver as investors seek assets that perform well amidst such economic shifts. The silver market is anticipated to experience its fourth consecutive year of deficits, with a minor decrease expected to reach 176 million ounces. Various factors, including production and industrial offtake, will influence the deficit forecast, potentially maintaining high deficits…

Read More: Global Economic Shifts and Their Impact on Silver as a Dual-Asset – Resource