“Rising breakeven prices reflect the increasing cost pressures on the upstream industry. This challenges the economic feasibility of some new projects, but certain segments, including offshore and tight oil, continue to offer competitive costs, ensuring supply can still be brought online to meet future demand. Managing these cost increases will be critical to sustaining long-term production growth,” said Espen Erlingsen, head of upstream research at Rystad Energy.

From 2014 to 2020, tight oil and OPEC were the clear winners, as both segments saw a reduction in the breakeven price and an increase in potential volumes, according to Rystad. Since 2020, the potential supply from tight oil has been reduced, and Rystad now expects tight oil to produce around 22 million b/d by 2030, including natural gas liquids (NGL). The reduction in future tight oil supply is caused by the change in company strategy, with more cash paid out to investors and amid industry consolidation.

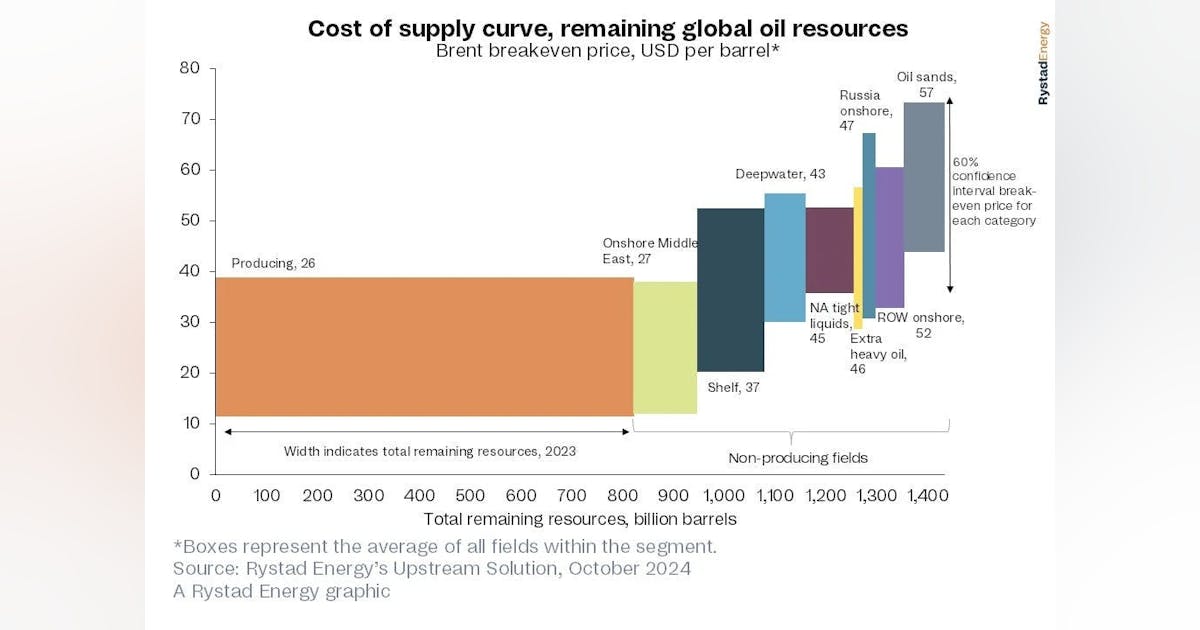

Between 2014 and 2020, the offshore shelf and deepwater sectors experienced a cost reduction of around 35%. However, the lack of new sanctioning activity over the period reduced the potential 2030 offshore liquids supply. Compared with 2022, breakeven prices for the deepwater and offshore shelf segments are rising due to higher unit prices. Oil sands, however, continue to see a reduction due primarily to the lower observed operational costs for this heavy oil segment, Rystad said.

Beyond breakevens, average payback for new projects, internal rate of return (IRR) and carbon dioxide (CO2) intensity are vital metrics for evaluating new oil development economics. The tight oil sector’s payback time is just 2 years, assuming an average oil price of $70/bbl, illustrating how quickly operators are recovering their investments, Rystad said. Payback time is closer to 10 years or more for the other supply segments. Tight oil also leads the pack in terms of IRR, with an estimated IRR of around 35% in the same average oil price scenario. Conversely, oil sands, the most expensive supply source, has the lowest IRR of about 12%, according to Rystad research.

Over the last 3 years, the average CO2 intensity for tight oil has been 14 kg/boe, while deepwater has a slightly higher average CO2 intensity of 15 kg/boe. The oil sands sector holds the highest future estimated emissions at around 70 kg/boe, according to Rystad Energy.

Read More: Rystad Energy: Cost of new upstream oil projects rises further