Rate cuts cannot fix the structural issues crushing office & retail CRE. But industrial, fueled by ecommerce, is in good condition.

By Wolf Richter for WOLF STREET.

Maybe Commercial Real Estate has hit “bottom” – as property giant Blackstone’s president and chief operating officer, Jonathan Gray said in January during an earnings call, which then was echoed by other CRE fund managers with lots of troubles in their portfolios. Or maybe it hasn’t.

Parts of it are in deep trouble, such as office, retail, and lodging, including for structural reasons that have nothing to do with interest rates and cannot be cured with rate cuts. Multifamily is not in as bad a shape, though problems abound amid numerous defaults and oversupply in some markets (oversupply of housing is exactly what consumers need, so this is a good thing for the economy but not for lenders and investors). And industrial, such as warehouses and fulfillment centers, is in good shape, though the bloom has come off the rose too.

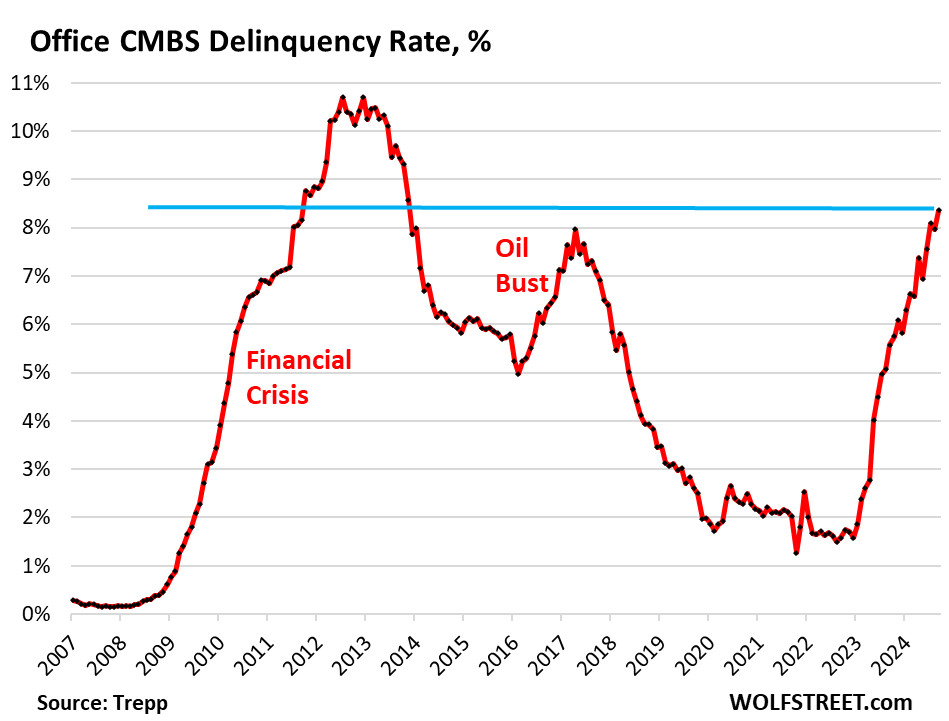

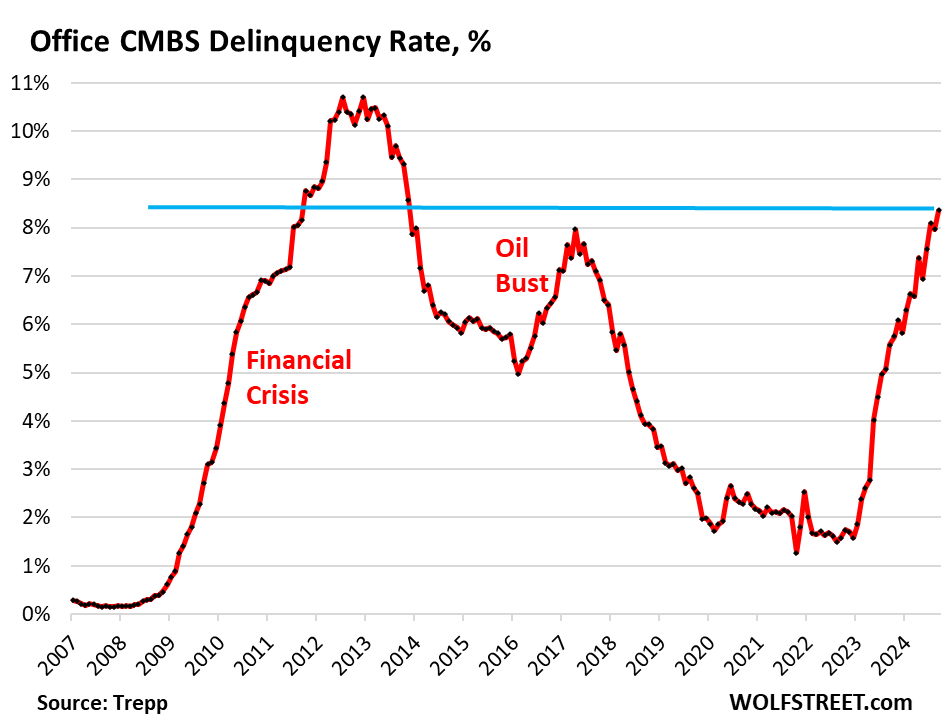

Office CMBS.

Delinquency rates of office mortgages backing commercial mortgage-backed securities (CMBS) spiked to 8.4% in September, the highest since the peak years of the Great Recession from August 2011 through November 2013, according to data by Trepp today, which tracks and analyzes CMBS.

The delinquency rate has now surpassed the spike that followed the American Oil Bust from 2014 through 2016, when hundreds of companies in the US oil and gas sector filed for bankruptcy, which devastated the Houston office market in 2016.

The office sector of CRE faces a structural problem: A huge office glut after years of overbuilding amid massive hype about the “office shortage” that led big companies to hog office space as soon as it came on the market with the hope they’d grow into it. Now companies realize that they don’t need all this office space, and vast portions of it sits there vacant and for lease. Rate cuts will do nothing to address these structural issues, though they might help some borrowers refinance a maturing loan on a building with adequate occupancy.

Mortgages are considered delinquent by Trepp when the borrower fails to make the interest payment after the 30-day grace period. A mortgage is not included here if the borrower continues to make the interest payment but fails to pay off the mortgage when it matures. This kind of repayment default, while the borrower is current on interest, would be on top of the delinquency rate here.

Loans are pulled off the delinquency list if the interest gets paid, or if the loan is resolved through a foreclosure sale, generally involving big losses for the CMBS holders, or if a deal gets worked out between landlord and the special servicer that represents the CMBS holders, such as the mortgage being restructured or modified and extended.

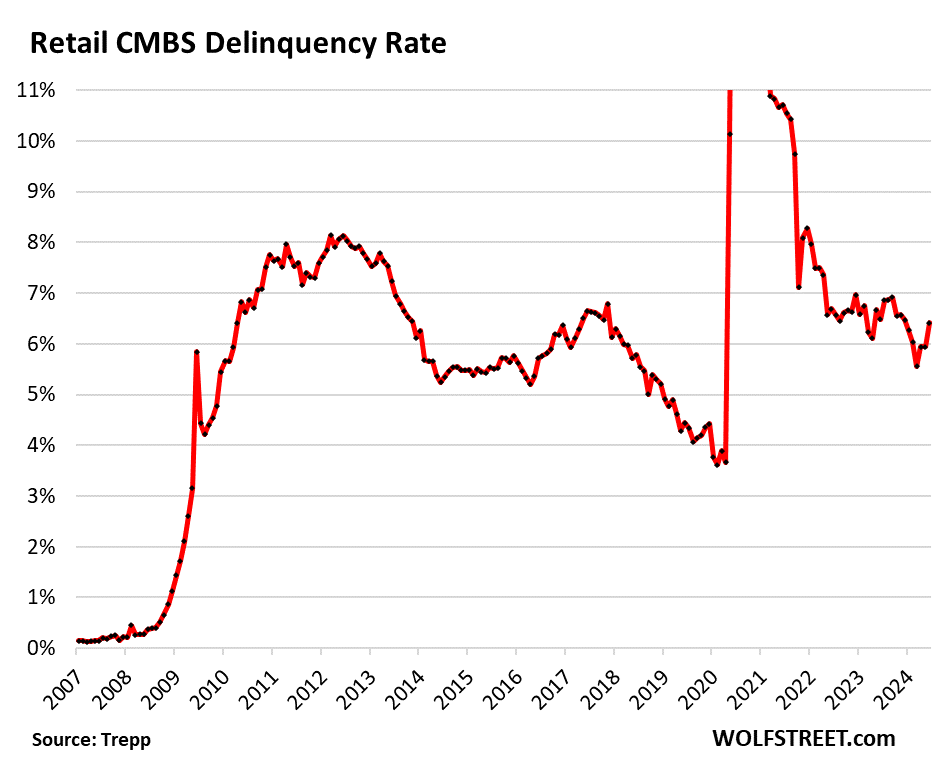

Retail CMBS.

The delinquency rate for mortgages backed by mall properties spiked to 7.1% in September.

Mall properties and other retail properties have been in trouble for years, as ecommerce is taking their business away, a phenomenon that we’ve called the Brick-and-Mortar Meltdown since 2016. And even the big mall landlords have all been defaulting on mall loans and letting the affected property go back to lenders.

For example, Simon Property Group [SPG], the largest mall landlord in the US, has trimmed its mall count for over a decade, including by defaulting on mall loans and walking away from several properties. In June, it began walking away from another mall, the second largest mall in Pennsylvania, the 1.7 million square-foot Philadelphia Mills outlet mall. The loan came due, and SPG failed to pay it off. In July, it emerged that it was negotiating with the special servicer to hand the property back to the CMBS holders.

Countless retail chains, from Sears on down, filed for bankruptcy, and many were liquidated. Zombie malls sit abandoned until a developer can bulldoze the buildings and build housing on the property.

This is the structural problem of brick-and-mortar malls, as Americans have changed their shopping patterns with a relentless shift to ecommerce. Department stores have been totally crushed, with only a handful of survivors that have all slashed their store counts of the years.

No rate cut ever is going to stop ecommerce from continuing to take over a big part of the retail business.

Exempt from the meltdown have been strip malls anchored by grocery stores, and service establishments and restaurants among the other tenants.

Lodging CMBS.

The delinquency rate for mortgages backed by hotel and resort properties rose to 6.2% in September, after declines in the prior two months.

During the pandemic, when many hotels were shut down for a while, the delinquency rate had spiked to 24% in June 2020….

Read More: CRE Mess Not Letting Up: CMBS Delinquency Rates Jump in September as Office,