(Bloomberg) — A previously gloomy corner of the debt world has become the biggest winning trade in global financial markets, producing returns that few traders have seen in more than a decade.

Most Read from Bloomberg

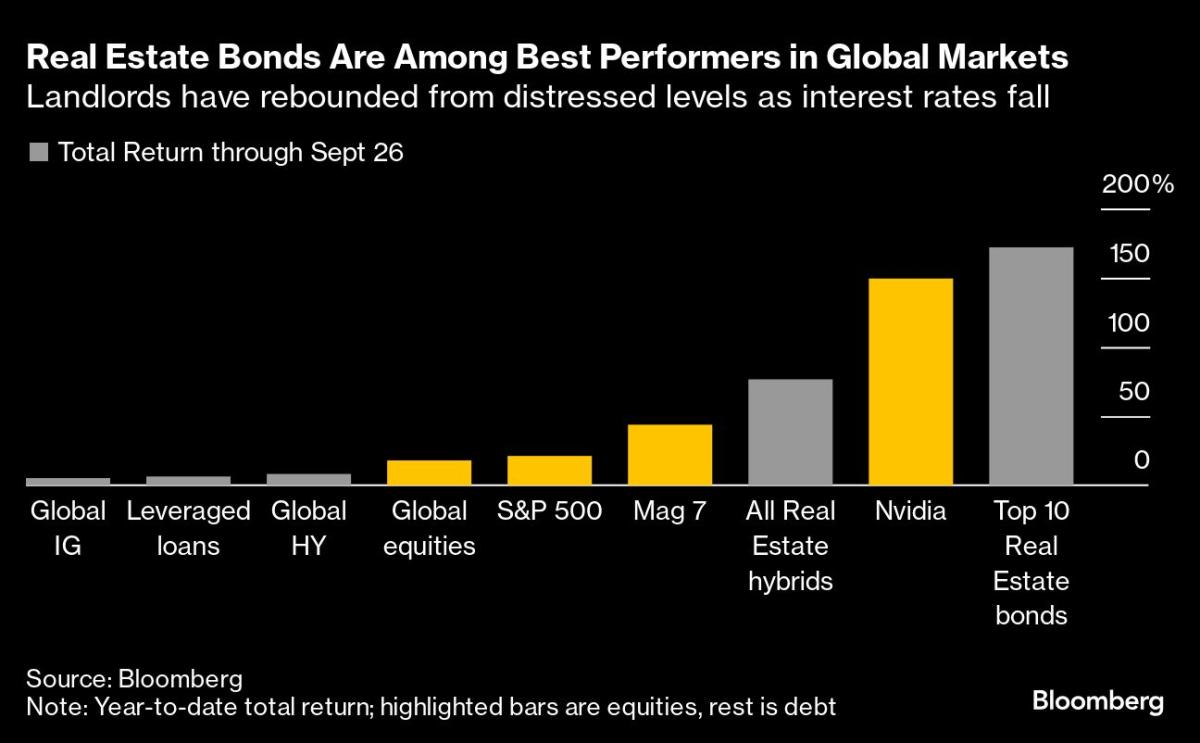

Hybrids, the riskiest slice of a real estate company’s debt, have returned more than 75% this year. For the top 10 performers for the securities also known as subordinated bonds, returns amount to about 170% in the period, beating Nvidia Corp.’s stock, the darling of the AI craze, by 20 percentage points.

It’s the kind of swift turnaround that few could have predicted when landlords around the world were creaking under the weight of higher interest rates and changing work habits following the Covid-19 pandemic. Now, real estate debt is becoming an early winner from major central banks cutting borrowing costs amid a pivot to prioritizing the economy over battling inflation.

“I cannot recall something similar in my career,” said Andrea Seminara, chief executive officer at London-based Redhedge Asset Management, who started working in finance at the height of the global financial crisis in 2008. “The magnitude of the gains is unprecedented, unless we look at pure distressed situations.”

Replacement Cost

Landlords’ subordinated bonds had plunged nearly 50% after central banks began to increase rates in 2022. Higher borrowing costs meant the cost to replace them shot up, leaving investors fearful that repayment would be delayed indefinitely.

Companies can also sometimes skip coupons on the notes without triggering a default, making them less popular with investors.

“These bonds were punished due to technical factors,” said Andreas Meyer, founder of Hamburg-based Fountain Square Asset Management. “There was blood on the streets.”

For Seminara, buying at those depressed levels was effectively a bet that companies would be able to replace debt that was coming due and that falling inflation would allow central banks to cut interest rates. Both proved correct.

The companies faced a so-called maturity wall that collapsed in historic fashion this year as capital flowed into the credit market, allowing landlords to issue new debt to refinance old bonds. Meanwhile, the Federal Reserve this month joined the European Central Bank and the Bank of England in cutting its policy rate and leaving open the possibility of further large cuts.

Meyer’s event-driven fund is among those that reaped the benefits, gaining as much as 80% in its hybrid bonds. He still has exposure in the sector.

The main risk now is that there is little juice left in the trade. Strategists Barnaby Martin and Ioannis Angelakis at Bank of America Corp. flagged in a report last week that “valuations are clearly nearer to becoming full” in real estate credit.

Still, buyers and sellers are becoming more confident that the commercial real estate market is bottoming out. Many want to start putting capital to work as the interest rate pain starts to ease.

“We have lived through a sh*tstorm. No one has lived through a monetary policy as aggressive as we have seen in the last two years,” Madison International Realty founder Ron Dickerman said in an interview. “A couple of rate cuts does not make a market, but there’s optimism.”

Week in Review

-

China disclosed a series of stimulus measures designed to boost flagging growth in the nation. It unveiled its biggest package yet to shore up its beleaguered property market, lowering borrowing costs on as much as $5.3 trillion in mortgages and easing down-payment requirements for second home purchases to a historical low.

-

China is also considering injecting up to 1 trillion yuan ($142 billion) of capital into its biggest state banks to increase their capacity to support the struggling economy.

-

While some details are missing, the unusual pace and intensity of the stimulus announcements signaled a sense of urgency in Beijing to put growth on track for the around 5% target, buoying market sentiment.

-

Separately, the nation began marketing its first euro-denominated bond in three years.

-

-

US companies and Asian issuers stormed debt markets following the Federal Reserve’s decision last week to lower its benchmark interest rate by half-a-percentage-point.

-

A resurgence in mergers and acquisitions dealmaking is turbocharging the US high-grade bond market to its fastest pace of issuance since 2020, putting it on track to post $1.5 trillion of sales.

-

Banks and other lenders are lining up more than €10 billion ($11.1 billion) of debt to back a buyout of Sanofi SA’s consumer health division, as one of the most hotly-anticipated sales of the year reaches its final stages.

-

Blue Owl Capital Inc. led the $3.2 billion private debt financing supporting Blackstone Inc. and Vista Equity…

Read More: Riskiest Real Estate Bonds Are Beating Nvidia’s Returns