(Bloomberg) — The feared maturity wall is proving more of a speed bump, with the world’s junk bond market so far this year seeing the biggest decline in looming debt repayments in at least a decade.

Most Read from Bloomberg

Since the start of 2024, corporates have settled just over $170 billion of their high-yield bonds due in the coming two years, according to data compiled by Bloomberg. That’s more than they redeemed over the entire course of 2021, when repayments peaked amid rock-bottom financing costs.

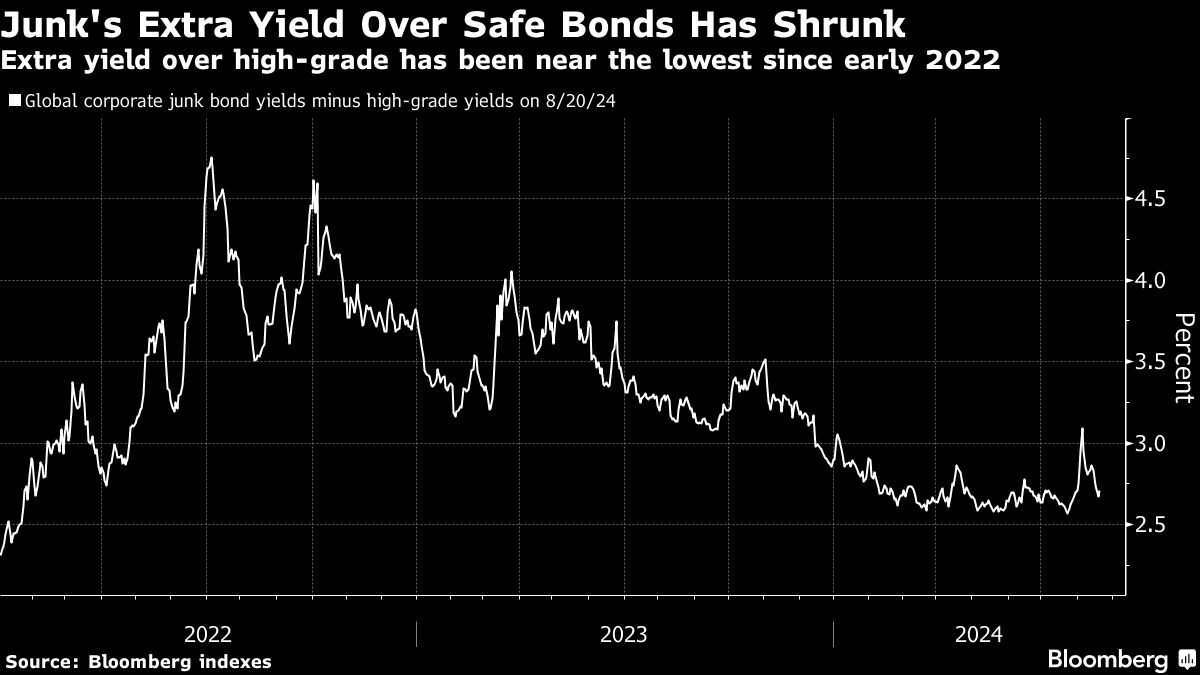

The erosion of the maturity wall — market parlance for a large amount of debt coming due at the same time — is alleviating worries about a potential wave of defaults. Risky borrowers are refinancing at higher interest rates, shaking off concerns that they’d be saddled with unsustainable debt costs, leading to bankruptcies and firings with knock-on effects for the real economy. Instead, investors trying to lock in yields ahead of anticipated interest rate cuts have bolstered demand, keeping spreads down.

This “is less of a wall now. Maybe a fence,” said George Curtis, a portfolio manager at TwentyFour Asset Management. “The market has been in a pretty good place. Macro has been more stable, while the high yield market has seen decent inflows.”

Firms typically try to refinance maturing debt about 18 months before it comes due to avoid any sudden shutdowns in new issue markets that could scupper their plans at the last minute.

They’ve been able to count on investors’ eagerness to buy the debt of risky issuers, as leveraged loan funds recorded $11 billion of inflows this year through Aug. 7, according to LSEG Lipper data. High-yield notes had net inflows of about $680 million in the week ended Aug. 21, the provider said.

That’s helped make 2024 the busiest year for issuance of new corporate high-yield bonds, with $357 billion sold so far, since the easy money days during the pandemic. Issuance of US leveraged loans, meanwhile, is running at its fastest pace on record, data compiled by Bloomberg shows. Combined, that’s helped push the maturity wall out to the end of the decade.

Private equity company EQT AB has been among those taking advantage of the demand from investors to refinance the debt of companies they own.

“Over the past 12 months, we have executed more than 20 maturity extensions across the portfolio,” said Olof Svensson, head of shareholder and bondholder relations at EQT, during its latest earnings call.

An additional factor playing into the hands of borrowers is the appetite coming from the $1.7 trillion private credit market, which has given borrowers more refinancing options.

“Resurgence of the high yield and leveraged loan primary markets is one thing, but private credit bid has previously helped and is ongoing,” said Marco Stoeckle, head of credit strategy at Commerzbank AG.

Click here to listen to the Credit Edge podcast on private credit in Europe

To be sure, the sudden surge of volatility in early August is a reminder of how vulnerable credit markets are to growth scares. The cost of protecting a basket of North American junk debt against default shot up to its highest level this year before recovering.

Still, major central banks look set to embark on a rate-cutting cycle, with traders pricing in close to four 25-basis-point cuts by the Federal Reserve until the end of the year.

“Given the improved rates momentum, the funding outlook is no longer as toxic as in large parts of 2022 and 2023,” said Commerzbank’s Stoeckle.

Week in Review

-

The Federal Reserve’s widely expected pivot to lower interest rates next month is creating a conundrum for one of the biggest winners of the high-rate era: private credit. While easier monetary policy will come as a relief to borrowers with heavy debt loads, it’s also set to sap the returns of an industry that boomed as rates rose.

-

While credit markets rally in anticipation of lower interest rates, junk bond guru Marty Fridson warns that risky debt may underwhelm.

-

ESG bond sales from US-based firms are running at the slowest pace since 2019 as politics and the lack of price benefits make them less practical.

-

Kroger Co. sold $10.5 billion of notes to help fund its acquisition of fellow grocer Albertsons Cos. in one of the biggest corporate bond deals of the year.

-

Retail investors are caught in the crossfire of B. Riley Financial Inc.’s downward spiral. The beleaguered firm used an unusual debt product known as baby bonds to raise cash from small-time investors. Now, their money is at risk.

-

A mainland Chinese court accepted a liquidation application filed against a China Evergrande Group unit earlier this month, triggering a formal legal process that ratchets up the pressure on the defaulted developer to either…

Read More: Junk Bond Maturity Wall Erodes as Money Managers Seek Yield