matdesign24/iStock via Getty Images

In keeping with my coverage on bonds and bond trends, I thought to write a quick article on recent trends impacting high-yield bonds as an asset class. Three trends stand out.

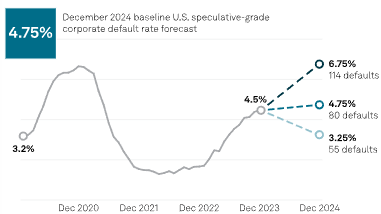

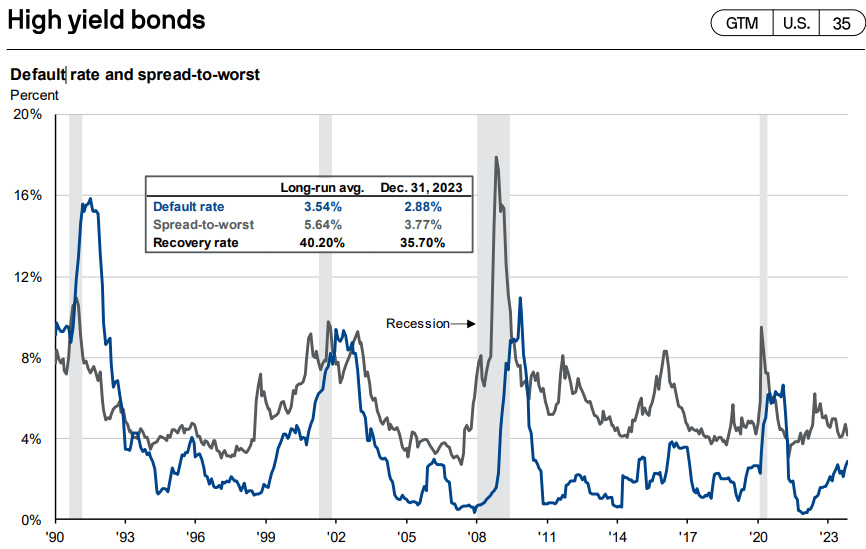

Default rates are rising, reaching 4.5% this past December. Analysts expect defaults rates to continue rising, but only slightly so.

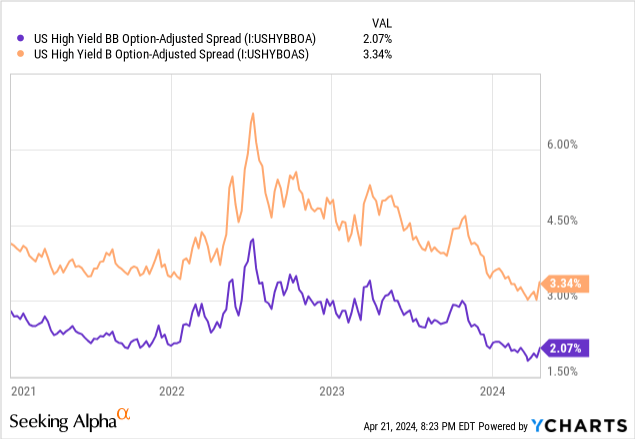

Credit spreads are narrowing and are currently below historical averages. For bonds rated BB, spreads currently stand at 1.9%.

Due to the above, prospective risk-adjusted returns for high-yield corporate bonds look quite weak. Treasuries look much better, investment-grade bonds too, but less so.

In my opinion, high-yield bonds still have a place in an investor’s portfolio, due to their high yields and as economic conditions remain adequate. Fundamentals are worsening though, which might be a deal-breaker for many investors.

I’ll be focusing on the iShares iBoxx $ High Yield Corporate Bond ETF (NYSEARCA:HYG) for the remainder of this article, as this is the largest high-yield corporate bond fund on the market. I much prefer other funds though, including the SPDR Portfolio High Yield Bond ETF (NYSEARCA: SPHY) and the iShares Broad USD High Yield Corporate Bond ETF (BATS: USHY).

HYG – Quick Overview

HYG is a simple high-yield corporate bond ETF, tracking the Markit iBoxx USD Liquid High Yield Index. It is a relatively simple index, including all bonds with the following characteristics:

- fixed-rate

- developed market corporate issuer

- dollar denominated

- non-investment grade credit rating, BB or lower

Applicable securities must also meet other basic inclusion criteria centered on liquidity, size, and the like.

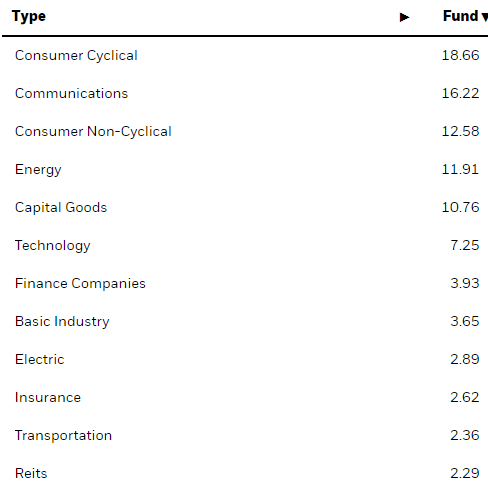

HYG is an incredibly well-diversified fund, with investments in over 1,000 securities, and with exposure to most important industries.

HYG

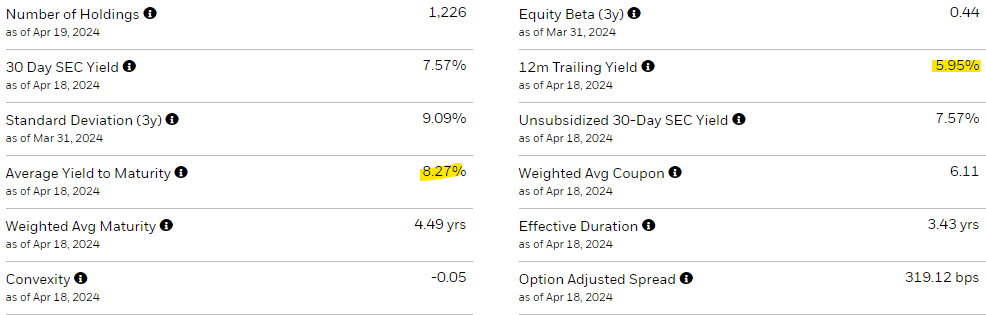

HYG currently yields 6.0%, a respectable yield, but somewhat lower than expected for a high-yield bond fund. This is because it still holds older bonds from when rates were lower. Although these have lower yields, their prices should rise as they mature. HYG’s yield to maturity of 8.3% takes into consideration these potential price gains, and is much more reflective of the returns investors should expect moving forward.

HYG

HYG is diversified enough to function as a stand-in for the broader high-yield bond market. With this in mind, let’s have a look at recent trends impacting these securities and HYG.

HYG – Recent Trends

Rising Default Rates

High-yield corporate bond default rates have risen, from around 3.2% pre-pandemic to 4.5% as of December 2023. Analysts expect default rates to rise even further this year, as higher rates continue to impact the finances of many companies.

S&P

Higher default rates are a straightforward negative for high-yield corporate bonds in general, and for HYG. Higher default rates also increase the attractiveness of investment-grade securities vis a vis high-yield bonds. Treasuries are not impacted by default rates, so treasuries look stronger as default rates rise.

Tighter Credit Spreads

High-yield corporate bonds consistently yield more than investment-grade bonds of comparable maturities, due to their added credit risk. Spreads do vary, depending on underlying economic conditions and investor sentiment. Spreads have decreased by around 3.0% since their mid-2022 highs, by around 1.0% since early 2023.

Spreads are currently around 1.0% lower than their medium-term averages, almost 2.0% lower than the long-term average.

JPMorgan Guide to the Markets

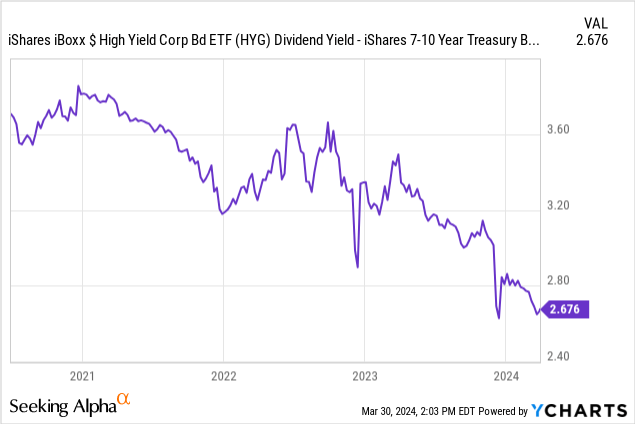

Spreads between HYG and benchmark treasury ETFs have also tightened, consistent with the above. Spreads are down around 1.0% these past few years, reaching their lowest levels in history.

Data by YCharts

Tighter spreads are an obvious negative for high-yield corporate bonds in general, and HYG in particular. Tighter spreads also increase the attractiveness of investment-grade bonds over high-yield bonds. If treasuries yield almost as much as HYG, might as well focus on the safer, higher-quality treasuries. Higher default rates tilt the scales further, which brings me to my next point.

Weaker Risk-Adjusted Yields and Returns

Right now, high-yield corporate bonds seem to offer weak risk-adjusted returns. Risks are higher, or more salient perhaps, due to elevated interest and default rates. Returns are lower, insofar as spreads are tighter. This is a terrible combination for high-yield corporate bonds, and although neither defaults nor spreads are at disastrous levels, both figures are quite poor, and trending worse.

An implication of the above could be to simply avoid high-yield bonds altogether. I’m not sure that I would go so far. High-yield bonds continue to offer, well, high yields, and the broader economy remains strong. High-yield bonds…

Read More: 3 Trends Impacting HYG And High-Yield Bonds